Whether one likes it or not , in this new era of protectionism and domestic value capture, India needs a smart Industrial Policy to grow its manufacturing sector and exports. Exports have fallen since 2013, and our manufacturing sector is facing stress, having grown at a compound annual growth rate (CAGR) of barely over 4% since 2011. Since China implemented a successful Industrial Policy, its economy has grown to become 4.5-5 times larger than India’s. Many other market economies including Japan, the United States and South Korea have implemented effective Industrial Policies at different times, all the free market rhetoric notwithstanding, and there are lessons to be learnt from each model. An Industrial Policy is not incompatible with a market economy – it, in fact, “crowds in” private sector investment and growth, as Prof. Mariana Mazzucato has detailed in her works on the role of the State in encouraging innovation and creating new sectors and opportunities for growth.

In the context of aerospace manufacturing, the recent announcements by the Commerce and Industry Minister about launching an Industrial aircraft manufacturing policy, coupled with the Draft Defence Production Policy and related reforms in defence procurement, provide an opportunity to launch a full-fledged, uniquely Indian Industrial Policy. We have one great advantage over China: a vibrant private sector whose potential we have neither fully unleashed nor exploited. By making it a full and respected partner in development, we can achieve new heights. This is something China is also realizing as it is trying to give greater autonomy to its state-owned enterprises. An Industrial Policy in tune with the market will thus yield massive dividends.

India’s manufacturing sector under stress

Merchandise exports have fallen from US$336 bn in 2013, to just over US$ 260 bn in 2016. Between FY12 and FY18, India’s manufacturing sector saw Compound Annual Growth Rate of only 4.34%[i].Perhaps this is the reason behind the pessimism of recent articles and Government reports that downplay the prospects for Indian manufacturing – this year’s Economic Survey even left out the chapter on manufacturing. However, despite headwinds and domestic macro-economic shocks, manufacturing – which makes up only around 16% of GDP – still accounts for 68% (or US$ 180 bn) of total merchandise exports. Services, on the other hand, which account for around 55% of India’s GDP, produce only 38% of its exports (2016). Therefore, 16% of our economy is essentially still producing more exports than 55% of our economy, underlying the higher value addition for the economy as a whole, that manufacturing still provides.[ii]

However, a mainstream website has put it like this: “India’s share in global services exports stood at 3.2% in 2014-15; double that of its merchandise exports in global merchandise exports at 1.7%”[iii]. But global services exports were not even 1/3rd of global manufacturing exports of US$ 16 trillion that year. Statements like these are often misleading because, like this one, they leave out important details.

The need

India’s economy is not so much services-led as it is manufacturing-deficient. India cannot afford to forget that the value multiplier of manufacturing is greater than that of services. Manufacturing’s role in increasing the population’s purchasing power and securing better terms of trade has never been questioned by serious economists. A high-tech manufacturing sector is also crucial for the national security of a country like India aspiring to greater geopolitical status. Neglecting the manufacturing sector carries the danger of falling further behind China. And the development of high-end service industries in India is also contingent upon India’s embrace of Industry 4.0 driven by artificial intelligence and embedded technologies. India may actually lose its current advantage in IT services if it doesn’t keep pace with technological advances in manufacturing.

Moreover, since key services sectors such as telecom and aviation depend overwhelmingly on equipment imports, their contribution to the economy is dampened due to the concomitant negative impact on India’s current account balance. We must consider imposing obligations on the services sectors to support R&D and manufacturing through direct investments or levies like the universal service obligation (USO), which, currently, remains sub-optimally utilized. This is particularly important as India’s current account deficit (CAD) is widening again due to the oil price rise, and volatile capital flows are placing the rupee under pressure.

We need an Industrial Policy to help India’s manufacturing sector achieve its full potential. This will enable India to source a major part of its high-tech equipment requirements – including defence, aircraft, electronics, telecom and rail – domestically, leading to a permanent structural reduction in the CAD., maximum value addition within the country’s borders, and to integrating India at the top-most end of high-value global manufacturing supply-chains. The other multipliers, including positive social, security and military spin-offs, are self-evident.

Many market economies have adopted Industrial Policies, so there is no need to be apprehensive that India is in danger of reverting to Licence Raj. The recent Ministerial announcements on an Industrial Policy and an aircraft manufacturing policy and the draft Defence Production Policy provide the perfect opportunity for action.

China’s Industrial Policy

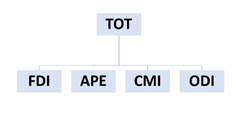

China realises that Technology is the Key to Comprehensive National Power. It has adopted a well thought out Industrial Policy to grow its own economy, the aim of which is to gain dominant market share in high value sectors by developing and acquiring advanced technologies[iv]. Its strategy can be summarised with the following acronyms – (i) TOT, (ii) FDI, (iii) APE, (iv) CMI & (v) ODI (Transfer of Technology; Absorb, Produce & Export; Civil Military Integration and Overseas Direct Investment), with technology-driven growth being the overarching goal of Industrial Policy[v].

FDI: Contrary to prevalent assumptions, China did not hold the door wide open to FDI after 1995, the way India has done[vi]. China has been regularly revising the Catalogue of Guidance for Foreign Investments and classifying the investments it allows, encourages, restricts and prohibits, in tandem with its stage of development. The OECD listed China among the most restrictive economies for FDI, but China still received US$ 168 bn in 2017 in FDI. China also frequently compels companies to part with technology by stipulating that FDI can enter only through JVs, or by ensuring TOT by foreign companies through administrative means. FDI policy thus reflects the dynamic changes in, and reinforces the technological upgradation, of its economy.

Our indiscriminate welcome of FDI, on the other hand, has led to most of it coming into the services and brownfield manufacturing sectors instead of the more advanced greenfield manufacturing areas. However, the draft industrial policy now seems to recognise that FDI hasn’t led to domestic value addition and has instead had “minimal positive externalities… Benefits of retaining investments and accessing technology have not been harnessed to the extent possible. FDI policy requires a review to ensure that it facilitates greater technology transfer, leverages strategic linkages and innovation”[vii].

The Chinese realised this when they first started controlling FDI, after an initial period of indiscriminately welcoming FDI inflows. Yet we hesitate to tailor FDI to our national requirements because our domestic industry is not investing, rendering India dependent on FDI. But a few tweaks – such as adding greenfield investment and TOT requirements in sectors where we want technology, encouraging greenfield, high-tech manufacturing investment and removing the automatic FDI brownfield investment route in sensitive and high-value areas like defence and pharma – will achieve the necessary impact. Otherwise, we shall continue to see our crown jewels in sensitive fields like pharma and e-commerce slowly slip into Chinese and foreign hands. The accompanying trend of excessive financialization of our economy may pander to neoliberal ideologies, but it spells disaster for balanced development.

Also, domestic reluctance to invest needs to be tackled on a war footing.

APE: The Chinese reportedly call their technology indigenisation policy – IDAR (Introduce, Digest, Absorb, and Re-Innovate)[viii], but years ago I came up with the acronym APE – or Absorb, Produce, & Export (pun intended). This policy encourages the Chinese to copy, reverse engineer and re-innovate imported technology.

CMI: This is the Civil Military Integration strategy, which has helped the Chinese divert technology acquired through the civilian sector, to the military. CMI also helps synergise the two sectors, as the increasing complexity of high-tech production means that there are no clear-cut lines between the civil and military sectors. Moreover, according to Prof. Tai Ming Cheung, modern economies witness a spin-on effect – the civilian sector is spinning on more technology to the military, than vice versa. In less advanced economies, it is the public-sector which has generated more technology. India is still witnessing mostly the spin-off stage.

ODI: Related to APE and CMI, is ODI, through which China unleashed a wave of high-tech acquisitions, leading to a sharp reaction. US Presidents cut off access to key technologies, and the Committee on Foreign Investments has placed Chinese high-tech ODI under greater scrutiny, with even Europe waking up to the dangers of China buying up its crown jewels, something I had anticipated in 2011[ix].

Through these single-minded, techno-nationalist policies, China has succeeded in growing its economy, generating world-class beating technologies and companies, and capturing value within its borders. The surpluses at the State’s disposal has ensured funding for successive S & T and Industrial development plans.

If our goal is to become the No. 1 Technology Superpower, India needs to move forward aggressively to implement an Industrial Policy. It can do this without ruffling too many feathers if it fashions it in tandem with the market, because we retain one crucial advantage over China that has not been fully exploited: our private sector. In partnership with the public sector and the State, it can help free up India’s manufacturing potential and create an R & D intensive, technologically advanced economy.

New Industrial, Defence & Aircraft Production Policies

In this context, the Minister for Commerce, Industry and Civil Aviation’s announcement, Shri Suresh Prabhu’s announcement of manufacturing passenger aircraft and drones being one of his top priorities in 2018, is very timely. The announcement in March also outlined his vision to make India an aviation and cargo hub. He stated, “We do not want 1,300 planes to be bought from abroad. We will make them in India”. He also declared that a new Industrial Policy is being framed after 25 years and it is being designed to “equip Indian industry for the future” [x] The Ministry will hopefully “work together with its defence counterparts to look at civilian and defence aircraft requirements and [use] high end technology like artificial intelligence and robotics in the airlines industry will be another priority area for the ministry”[xi].

Civil Military Integration – Indian style

Meanwhile, the Ministry of Defence drafted the Defence Production Policy 2018 and listed leveraging “mutually beneficial links between military and civil aviation for expansion and, importantly, indigenisation”. It further stated: “Government will develop civilian aircraft of 80 to 100 seats over the next 7 years” and “Global majors will be encouraged to set up manufacturing capabilities of their platforms in India, both to cater to domestic needs and export from India.”

As a result, four key Ministries (Defence, Civil Aviation, Commerce & Industry) have announced their intention to work towards the common goal of building civilian and defence aircraft. This is unprecedented in India, in the context of the silo-based Indian ecosystem – it mirrors the Chinese practise of Civil Military Integration, a concept particularly apt for aviation, the technologies for which span the civil and military sector.

Aerospace Manufacturing Policies and Industrial Strategies of other countries

A big push in the aviation sector can be the basis for the launch of a new Industrial Policy to impart dynamism to India’s manufacturing sector.

China has a well-funded civil aerospace program. It has deployed the instruments detailed above but has been unable to match the capabilities of Boeing and Airbus. According to reputed analysts, aviation majors and component suppliers alike are withholding the latest technologies to forestall having these acquired or stolen. Hence, a policy based on coercion has not worked optimally for China. But this does not call for complacency: China has achieved several milestones in aerospace manufacturing, and is increasingly integrated in global manufacturing supply chains, leveraging its vast market in return for access to technology.

Japan also had an Industrial Policy to re-grow and restore its war devastated high-tech sectors, including its aviation industry. It has had greater success in integrating itself into global supply chains created by Boeing and Airbus: today, Japan supplies 35% of the Boeing 787, and more than 25% of Boeing, equipment. The US Industrial Policy is also worth examining – the US aviation industry could not have developed without applying the full might of the State’s resources, including funding, technology support and massive procurement.The current drive to reshore high-tech manufacturing pursued robustly by President Trump is in realisation of the efficacy of Industrial Policy.

The critics in India who scoff at Industrial Policy and deem it incompatible with the market, need to consider the benefits of such strategies. These strategies are followed by market economies across the world, including countries like Brazil, South Korea and Turkey who use a more stringent Offsets policy than India.

Going for the Sky

India must seize the opportunity presented by its burgeoning aircraft and aviation related market to promote its own companies and impart a strong growth momentum to its manufacturing economy. We have a huge market opportunity in civil and military aircraft (with Airbus projecting a demand for 1750 civil aircraft in the next 20 years), airport infrastructure and the MRO sector. We can leverage market access in each of these to help India advance high-tech aerospace manufacturing, and further integrate into global supply chains as a start, following a hybrid Japanese-Chinese-Brazilian model. For this, the Government must move forward with the Industrial Policy where the Indian Industry is an equal and respected partner.

India must realise that our one advantage over China is that we have a strong private sector, with many patriotic companies willing to do their bit to make India stronger. Undue suspicion of our own companies hurts only ourselves. India’s Industrial Policy can succeed if it relies on Indian Industry, including the private sector, in partnership with the State. The Industrial Policy should consist of the following:

- A strong Offsets policy for civil aviation (at present it is subsumed under Defence Offsets): Our offsets policy is one of the weakest in the world, as pointed out in our report[xii], with the highest thresholds and the lowest percentages (30%, against some countries’ 100%).

- A Buyers Consortium: It would be politic to retain Air India as a PSU after a thorough overhaul of its finances and business practices, so that it can lead the Buyers Consortium together with another PSU – HAL. Market access should be leveraged for technology payoffs with aviation majors. As Dr Ajay Kumar, Defence Production Secretary says “a strong public sector presence and strong private industry presence in various verticals of defence production would create healthy competition. We are working towards it”. This applies to civil aircraft manufacturing as well.

- Leverage the competition: China played off Boeing against Airbus and extracted many concessions for its domestic aerospace manufacturing program. And as Saurav Jha, Chief Editor of Delhi Defence Review has suggested, if India starts its own aircraft production program, there is every possibility that we will be courted with better offers for transfer of technology by aircraft majors.

- FDI, ODI and CMI: These instruments must be deployed for maximum technology absorption.

- A genuine PPP: We must dismantle all the obstacles the Indian industry has been facing and treat the patriotic Indian private sector as a respected partner in development.

- Proactive Science State: Industrial Policy can be fully compatible with the market, but given the scarcity of investible funds, the State must take the lead in opening new areas with investment in high-tech manufacturing and R & D, and share it with the private sector as a spin-off.

- PMA: The PMA must be extended to the Aerospace & Defence sector. This would be fully compatible with the proclaimed aims of the Government and the draft Defence Production Policy.

- Adopt US SBIR model for SMEs: Subventions should be given directly to SMEs along the highly successful US SBIR model. not routed only via incubators or Universities.

- Reorient CBI, CVC and CAG attitude to indigenous production: It must remove the culture of fear and vigilance by educating the CBI, CVC and CAG that patient finance[xiii] is required to develop indigenous, high-tech products.

- Issue a modern Defence Production Policy subsuming procurement: The Defence Procurement Policy is an anomaly and must be subsumed under a modern Defence Production Policy. No serious defence manufacturing country has such a Kafkaesque and elaborate procurement policy which defeats its own ends, severely penalising domestic producers; it should be made subordinate to indigenous production once and for all so that the accent is on production, not on procurement, which betrays an importing mindset.

- Services sectors like telecom and aviation to invest in R & D and manufacturing: We need to impose obligations on services sectors to invest in manufacturing, R & D and supporting innovative SMEs.

Going high-tech in the manufacturing sector is going to take patience with capital, in seeing outcomes, et cetera. We cannot afford to give up this quest even before it has begun by succumbing to defeatism. Only a very bold step forward will take the manufacturing sector to new heights, otherwise we will keep stagnating at the lower value end of the world economy.

Smita Purushottam has served as Indian Ambassador to Switzerland and Venezuela in the course of her career in the Indian Foreign Service. In the past, She also cut her teeth on India-China trade and investment issues while serving as Counsellor (Economic & Commerce) in the Indian Embassy in Beijing. After her recent retirement from the Indian Foreign Service, she has founded SITARA, a science & technology accelerator committed to aiding the commercialization of domestically developed technologies in India.

[i] https://www.ibef.org/industry/manufacturing-sector-india.aspx

[ii] http://stat.wto.org/CountryProfile/WSDBCountryPFView.aspx?Country=IN&Language=F.

[iii] Services Export From India: A Bright Future, Anu P. Mathai, IES, Chief Executive Officer, IBEF, Mar 28, 2017; https://www.ibef.org/blogs/services-export-from-india-a-bright-future

[iv] Findings of the Investigation into China’s Acts, Policies, and Practices Related to Technology Transfer, Intellectual Property, and Innovation Under Section 301 of the Trade Act Of 1974

https://ustr.gov/sites/default/files/Section%20301%20FINAL.PDF

“Technology as the Key to Power: What India can learn from China” in the book “Present Day China : A Net Assessment”, by Smita Purushottam, Observer Research Foundation China Studies Series #5, 2012

[v] This is broadly corroborated in the issue brief on “China’s Techno-nationalism”, presented to the US-China Economic & Security Review Commission on March 28, 2018, but I had come to the same conclusion while examining Chinese strategy, in the electric vehicles, aircraft, rail, and other sectors in a presentation I had made at BSDU on March 21, 2018.

https://www.uscc.gov/Research/china%E2%80%99s-technonationalism-toolbox-primer

[vi] Even during the pre-1995 honeymoon period, China had imposed some conditionalities for FDI to qualify for preferential treatment, such as export orientation or bringing in advanced technology.

[vii] Industrial Policy 2017 – A Discussion Paper: http://dipp.nic.in/whats-new/industrial-policy-2017-discussion-paper.

[viii] Findings of the Investigation into China’s Acts, Policies, and Practices Related to Technology Transfer, Intellectual Property, and Innovation Under Section 301 of the Trade Act Of 1974

https://ustr.gov/sites/default/files/Section%20301%20FINAL.PDF

[ix] “China woos Europe”, a prescient analysis. http://www.globalpolicyjournal.com/blog/14/02/2011/china-woos-europe-next-moves-eurasian-chessboard

[x] Feb 3 New industrial policy being ‘designed’ to equip industry for the future: Suresh Prabhu, IANS | Feb 03, 2018

[xi] “Govt wants to extend ‘Make in India’ plan to planes, drones: Aviation minister Suresh Prabhu” Business PTI Mar 14, 2018; https://www.firstpost.com/business/govt-wants-to-extend-make-in-india-plan-to-planes-drones-aviation-minister-suresh-prabhu-4390081.html

[xii] Report of the Fifth Meeting of the Forum on High-Tech Defence Innovation https://vistasbharat.wordpress.com/2015/03/09/report-of-the-forum-on-high-tech-defence-innovation

[xiii] Patient Finance is a term borrowed from the works of Prof. Mariana Mazzucato, Director of the Institute for Innovation and Public Purpose, University College London, to explain the long-term funding necessary for nurturing innovation.

© Delhi Defence Review. Reproducing this content in full without permission is prohibited.