Why India’s Release Of An Expression Of Interest For Semiconductor Fabrication Facilities Matters

Whether it be mobile phones or modern airliners, contemporary gadgetry and equipment are ultimately made possible through the use of semiconductors. And semiconductors are set to play an ever greater role as technologies such as the internet of things, 5G communications, autonomous vehicles, commercial robots and data centers become ubiquitous. It is therefore essential that India work quickly to create commercial scale manufacturing capability for semiconductors within the country. Not only is that a strategic necessity in this digital age, it would also enable India to become a top-tier manufacturing nation.

As such, India’s Ministry of Electronics and Information Technology (MeiTY) has brought out an Expression of Interest (EOI) “For Setting Up / Expansion Of Existing Semiconductor Wafer / Device Fabrication (fab) Facilities In India Or Acquisition Of Semiconductor Fabs Outside India ”. Perhaps enthused by the business response to its recent Performance Linked Initiative (PLI) schemes for mobile phone assembly, New Delhi at long last seems ready to backstop the augmentation of India’s electronics component manufacturing ecosystem.

It is well-known that a lack of significant indigenous electronic component fabrication in general and semiconductors in particular, has stunted domestic value addition in India’s electronics industry. Accordingly, one of the main strategies of India’s National Policy on Electronics 2019 (NPE 2019) is to facilitate the setting up of semiconductor fab facilities besides enhancing the ecosystem for the design and fabrication of integrated chips (ICs) and IC components on its soil.

Categorized into three distinct criteria, the EoI itself calls for proposals from ‘Established Integrated Device Manufacturers’ or ‘IDMs’, Semiconductor Foundries or consortia of companies with the capability to:

- Manufacture Complementary Metal Oxide Semiconductor (CMOS) based processors, memory, analog/digital/mixed-signal Integrated Circuits (Nodes below 28 nm, wafer size 300 mm and 30,000 wafer starts per month or greater)

- Manufacture High Frequency, High Power Optoelectronic devices (for cameras, sensors etc.).

- Acquire such semiconductor fabs overseas

Companies have been requested to elucidate possible site location, support requirements such as land, power, water, trained manpower, plant machinery, R&D support etc. The last date for submission of entries for the EoI is 31 January 2020.

Now, global semiconductor manufacturing majors include Taiwan Semiconductor (TSMC), Samsung (Korea), Global Foundries (UAE), United Microelectronics Corporation (UMC), Semiconductor Manufacturing International Corporation (SMIC, China), Tower Semiconductor (Israel-USA), Powerchip Technology Co., Ltd, Vanguard International Semiconductor (VIS), Hua Hong Semiconductor Limited(Hong Kong), Powerchip Semiconductor Manufacturing Corp (PSMC). Any Indian semiconductor foundry will likely be set up with the help of at least one of the non-Chinese entities (i.e. excluding SMIC for example) mentioned above.

In any case, the global demand for semiconductors is ever-increasing as we mentioned at the outset. For instance, The Semiconductor Industry Association (SIA) recently announced that the worldwide sales of semiconductors totalled $36.2 billion in August 2020, some 4.9 percent more than what was observed in August 2019. Furthermore, IC Insights reported in December 2020 that:

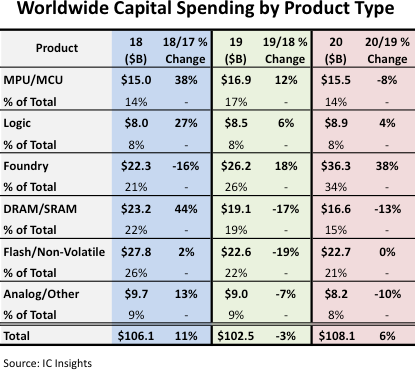

Following spending of $106.1 billion in 2018 and $102.5 billion in 2019, worldwide semiconductor capital spending is expected to grow 6% to $108.1 billion in 2020.As shown in the figure, the foundry segment is forecast to represent 34% of semiconductor capital spending in 2020, the largest portion of all product/segment types. Foundry also held the largest share of spending in 2014, 2015, 2016, and 2019.

Given these trends, India’s push for local data storage, data centers as well as high performance computing will create an increasing need for storage and computing hardware. Tech Insights reports that worldwide DRAM is forecast to experience a CAGR of 28.70% between 2018 and 2023. Capital expenditure of leading companies like TSMC hover around $15 billion, are matched by competitors such as Samsung planning a $116 billion expenditure in order to catchup with the former. TSMC’s revenues were $34.6 billion in 2019, while Samsung’s were $12.2 billion and GlobalFoundries’ reached $5.7 billion. It is high time India took the plunge to invest in such capabilities without baulking at the costs involved. Not doing so will involve far greater costs in the future.

© Delhi Defence Review. Reproducing this content in full without permission is prohibited.