As part of the World Trade Organization (WTO), India signed the Information Technology Agreement (ITA) in 1996. The ITA requires each participant to eliminate customs duties and bind them at zero levels for all products specified in the Agreement. The ITA covers a large number of high technology products, including computers, telecommunication equipment, semiconductors, semiconductor manufacturing and testing equipment, software, scientific instruments, as well as most of the parts and accessories of these products. The ITA and a benign neglect of the industry led to a floundering of the nascent existing ecosystem. A failure to recognize the importance of the sector and neglect of technology development, manufacturing and education/research ensured that post-2000, India was unable to develop a well-rounded electronics manufacturing sector. Just as worryingly, it has led to creating strategic vulnerabilities in fast moving technology sectors that the government will be slow to react to.

For instance, Silicon-based semiconductor manufacturing is a necessity for having a durable component manufacturing ecosystem. This enables local assembly of electronic products removing the need for import of semi-finished or finished products. India’s efforts to set up commercial semiconductor fabrication plants (fabs) have led to zero results as of date. Apart from low volume fabs that cater to the defence and space agencies, there is no bulk production facility in the country. Fabs are hugely expensive and cutting-edge production requires massive investments, not just in physical infrastructure but also in terms of technology, something that India continues to somehow not make.

China’s Path

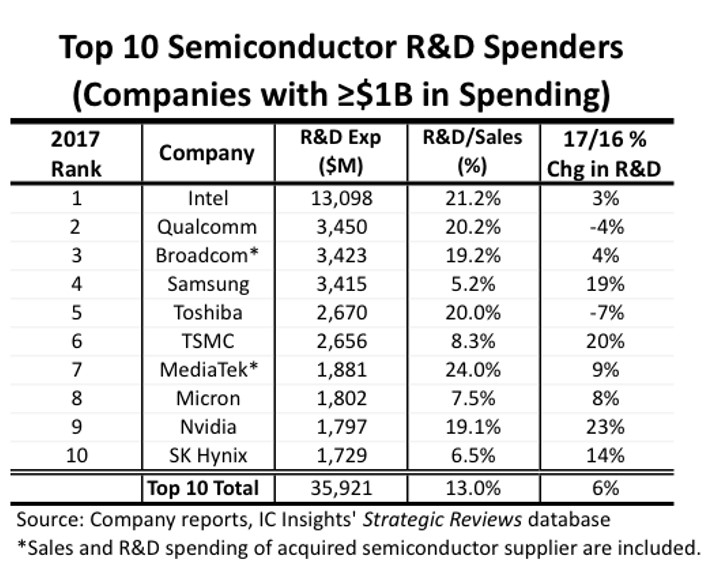

On a very different track, China entered the WTO from a position of strength, as a manufacturing powerhouse unlike India. The difference between China’s growth and India’s lag under ITA cannot be more stark and has actually been analysed threadbare. An aggressive government that could negotiate hard from a position of strength enabled China to exact favourable terms under ITA-2. A broad-based program called ‘Made in China 2025’ (MIC 2025) is the latest in its series of steps to move up the value chain and spur greater innovation and gain strategic independence. Today, China has extensive semiconductor production infrastructure and is working to expand its production footprint at a serious rate. At the same time, there is an equally strong focus on developing fabless design capability. The progress made by the China is evidenced by the presence of two Chinese companies in the top 10 for the year 2017 in terms of semiconductor R&D spending.

The Chinese government continues to set challenging targets for industry while extending deep support to domestic chip design companies and manufacturers. For instance, the Chinese government has provided tax cuts to further incentivize semiconductor production. Of course, despite the rampant growth in its IC industry, China continues to rely on imports for semiconductors, especially at the high-end of the spectrum. In order to remedy the situation, China has adopted a multi-pronged strategy that includes, apart from acquisitions of overseas technology companies, an ‘active poaching’ of talent from nearby countries that have an abundance of it, such as South Korea, Japan and Taiwan.

This approach seems to be yielding results. In 2016, Chinese company Hygon obtained AMD’s Zen architecture IP through a convoluted joint-venture of THATIC with AMD and has now begun producing its own ‘Dhyana processor’ that many believe bears a remarkable resemblance to AMD’s EPYC processor. So China’s recent foray into critical component manufacturing in the computing sector is not just in memory but spans all aspects.

The agenda obviously is to provide a solid hardware back-end to aid the creation of end to end domestic platforms. Baidu, which plans to launch autonomous buses for Beijing, Shenzen and other cities, plans to inject $1.5 billion (bn) for R&D in its Apollo platform that is used for autonomous driving solutions. Baidu is also partnering with Intel to incorporate computer vision systems into its platform and other Chinese companies, like their American counterparts are also investing enormous sums into AI. TSMC aims to spend nearly $14 bn in research and development at its Hsichu facility to chart its future. Samsung plans to build its new $5.4 bn plant in Hwaseong to produce below 7 nanometre (nm) chips from 2019. SK Hynix will build a new plant in Wuxi, China in 2019 along with Wuxi Industrial Development Group, an investment firm run by the regional government. The plant will house a new 200 mm wafer analog foundry production line.

What is India doing now and is it enough?

Now even as China is clearly making a play for global leadership, India has only made real headway in the arena of attracting final assembly of smartphones to its soil. While much derided for hiking import duty on components, the Phased Manufacturing Programme appears to be yielding results in terms of lowering costs and nudging phone makers into moving more jobs into the country to avoid duty on fully imported products. Success in this arena has prompted the government to push for similar schemes in other electronic goods manufacture also.

A draft National Digital Communications Policy was released earlier this year inviting public comments. This was followed by approval by the Telecom Commission in July. One of the biggest impediments to smooth the business environment is a byzantine regulatory framework that this policy aims to reform. Common requests among companies willing to enter and grow in this sector are easier licensing, greater ease of doing business, and a predictable regulatory framework. The policy also involves setting up a National Fibre Authority with a $100 bn target for investment. It aims to ensure India’s digital sovereignty along with the creation of some 4 million new jobs by 2022, increase the contribution of digital communications to India’s GDP to 8 percent from the current ~ 6 percent in 2017 and provide Broadband access for all. Among its goals for 2022 are:

- Increase India’s contribution to Global Value Chains

- Creation of innovation led Start-ups in Digital Communications sector

- Creation of Globally recognized IPRs in India

- Development of Standard Essential Patents (SEPs) in the field of digital communication technologies

With the government seemingly aware of near-future trends, it appears Indian consumers will be able to reap the benefits of 5G and other technologies in the way of the post-2000 telecom boom. However domestic capabilities to develop intellectual property (IP) in these areas continue to lag massively. India has also been unable to create and nurture a domestic ecosystem to capitalize on this boom. A smattering of product companies like Tejas Networks and products arising from IITs such as routers and a nascent journey to a family of microprocessors are what India has in terms of indigenous domestic efforts at the moment.

The government has also begun to setup an Electronic Development Fund (EDF) to create an ecosystem of innovation and research and development (R&D). This is modeled as a “Fund of Funds” to “participate in professionally managed “Daughter Funds” which in turn will provide risk capital to companies developing new technologies in the area of electronics, nano-electronics and Information Technology (IT). The EDF will also help attract venture funds, angel funds and seed funds towards R&D and innovation in the specified areas.”

In the recent times, India has also been implementing preferential market-access (PMA) in the ICT sector but has come in for much criticism for lackadaisical execution of the same. In January 2017, DoT issued conditions for a list of Telecom products to be classified as domestic and given preference. In June 2017, it issued directives for public procurement to provide a 20 percent price preference to products 50 percent local content. In September ’17, MoE & IT added a list of cybersecurity products to the June order. However, these are all incremental steps and a much deeper change in the attitude towards indigenous electronic manufacturing is necessary.

Paeans to a distributed global supply chain not-withstanding, the growth of the domestic electronics system design & manufacturing (ESDM) sector needs far greater hand holding from the Indian State. A certain level of preference and support until domestic firms are able to compete globally is absolutely necessary without resorting to License Raj. While national consumer preference and low-cost service is good, the homegrown ability to deliver it is just as important as getting it from outside, given the strategic risks involved.

Much more needs to be done

Many sectors need to move forward with a coordinated strategy to make India self-reliant in the ESDM sector. Disjointed programs executed in fits and starts based on political whims will not lead to competitive status. Rather, it needs a bipartisan technology roadmap that will be followed independent of elections and politics de jure. Companies, the world over, repeatedly say that they seek a well-defined policy framework, assured smooth funding, government support for export and elimination of tariff barriers and reduction in bureaucratic hurdles for ease of business. In emerging, nascent sectors, incentives such as tax holidays will need to be given. For example, China is providing tax rebates as part of its MIC 2025 program for select sectors such as chip-making.

Since the early 1990s, grand plans have been made from time to time in the form of National Telecom policy (1994, 1999) to strengthen R&D and to build ‘world class’ manufacturing capability, but it has been of no avail on account of poor implementation. Earlier PMA policies were circumvented by deliberate procurement terms even by government bodies. The current government’s flagship LED program Ujala was intended to procure LED bulbs manufactured in India. However tender-winner Philips resorted to imports from China to make up capacity shortfalls, while promising to increase domestic production.

Now while the government’s push to enlarge local production of mobile telephones has started yielding results, as mentioned above, it must move towards creating an end to end eco-system for smart telephony if value has to be retained and purchasing power has to be increased. The importance and need for Indian-designed and made products cannot be emphasized enough. Time and again, the general lack of knowledge in Silicon Valley about local conditions in other parts of the world has shown up in how tech products ignore the needs and wants of entire sections of the global populace. The fact of Apple belatedly releasing a dual-sim phone, which has widespread demand in Asia, is an example of the same.

Indian equipment makers have long requested that PMA be made applicable to private telecom operators too. Even with PSUs however, large tenders requiring established vendor requirements etc. eliminate smaller domestic vendors anyway. Enabling such vendors to ‘price match’ L1 bids by taking into account fiscal disability is among the prime requests being made by small domestic players. After all, smaller local companies are unable to obtain similar discounts as larger firms due to lower order volumes from foreign component makers. Besides telecom PSUs, educational institutions under government, defence, critical infrastructure like banks, power sector, railways, gas, water, all need to be included within the ambit of PMA. The security aspect of this should not be ignored.

Importance of funding basic R&D in domestic institutes, setting up of testing facilities, setting up easily accessible funds to domestic companies for R&D and testing cannot be overstated. Programs such as IDEX, Startup funds etc. are a decent beginning but need to be more broad-based and expanded. Stopping the drain of local talent not only improves domestic capabilities but also prevents others from utilizing them. India, being a very risk averse country, needs to develop a risk appetite. It is vital that a bipartisan approach to developing a tolerance to failure when large sums of money are involved is adopted. R&D is not a sure shot that will always produce results. However even failed projects can provide learnings for future successful programs. In order to sweeten the deal, tax incentives to telecom companies that invest in domestic R&D programs need to be introduced. At the monent, India’s Per Capita R&D spending compared to USA, Japan and China paints a dismal picture.

Building up semiconductor/component manufacturing capability has longer lead times and a lower success rate in comparison to design capability which is why it is important to promote design led manufacturing and fabless design. As such, Indian companies have requested greater Modified Special Incentive Package Scheme (M-SIPS) funding ‘allowable limits’. Moreover, tax rebates for companies that invest in R&D spending have been actually been decreasing in the past few years. This trend needs to be reversed along with a reduction in red tape to enable less cumbersome procedures in approvals for accessing funds. India has lost out massively on providing manufacturing jobs in the past decade with ever increasing telecom imports and decreasing exports. SIP EIT support is available, but larger companies have crowded out the smaller ones. Making patenting simpler & cheaper with funding support for small companies is of vital importance to create a wide ESDM base.

Given India’s massive market, anti-dumping measures should be used for equipment such as 4G/5G/Broadband systems/SDR/DWDM/IoT/Routers/Switches. Smart Cities, Digital India, IoT and other future interconnected technologies need massive physical infrastructure. India’s fibre optic infrastructure demand is expected to increase tremendously given the advent of 5G. BharatNet is an example of ample investment and project execution done on the back of domestic capability in the form of multiple optical fibre cable (OFC) producing companies. India also needs to leverage G2G deals to use ‘Make in India’ (MII) products while delivering aid to other countries and create a permanent MII brand like the Chinese have done. There is a greater need to educate and encourage the diplomatic corps to hard-sell the country’s capabilities and products.

Once again, India has made a good start by enabling increased phone “manufacturing” on its soil. However domestic assembly with little or no value addition cannot be an end in itself. Given India’s size, she needs to aim wider and higher up the value chain. Moreover, Huawei’s attempts to gain ‘domestic manufacturer status’ by showcasing local assembly is a case for watching out against foreign companies gaining access to incentives for domestic companies and crowding them out of their own market space. Meanwhile, the increased import duty on components must be maintained, despite opposition as that will lead to greater value addition on India soil via local sourcing.

Semiconductor based components contribute to nearly 80 percent of the bill of materials for low value products, but this part of the chain is entirely absent in India at the moment. This actually disincentivises even foreign companies to source locally and participate in PMA. Even if they do, they have no incentive to invest in local R&D and this only serves to reinforce the technology import cycle with newer tech coming from abroad. Foreign companies also demand easier market access and stridently oppose PMA measures, even if they their home governments do the same, like in the form of the Buy America Act.

Support domestic talent generation and innovation

Another prime requirement for innovation is talent generation. Reforming STEM higher education (as well as general educational standards across the country) is a massive need that needs to be addressed by the Indian State at the earliest. While, the IITs have not made it into the list of top institutions in the world, Chinese universities have made substantial progress. However, for all the investment that China pours in, Tsinghua notes that they still face talent shortages. To tackle this, China is using the carrot of market access to force tech companies to enter into research collaborations with domestic companies and institutes in emerging tech. Qualcomm tied up with Baidu’s Paddle Paddle, to develop an alternate to Google’s Tensor Flow deep learning framework. We’ve also seen how Chinese companies lure experienced professionals from nearby countries with bigger compensation packages and perks.

Apart from the absence of domestic semiconductor based component supply, even domestic printed circuit board (PCB) manufacture has slowly been supplanted by imported PCBs in a lot of products. Huawei has started assembling them recently at its Chennai facility. India is the world’s second largest mobile market overtaking the US in 2017 and the second largest mobile manufacturer. However, the market is dominated by Chinese manufacturers who have edged out Samsung and Apple. With more and more people lifted out of poverty and increasing disposable incomes, demand for consumer electronics will only increase in India. Greater tech know-why, local value addition will lead to more forex savings, local investments and the creation of high skill jobs. Moving up the value chain must be one of India’s prime National goals.

Telecom operator influence has led to massive imports of telecom hardware without commensurate investment in R&D, ecosystem development by way of investment in local manufacturing capacity. ‘Global ecosystem, supply chain’ glib-talkers leave out the reality of tech osmosis. In July this year, Xilinx purchased deep-learning startup DeePhi that builds advanced driver-assistance systems (ADAS). Backed by Xilinx, they were able to enter the commercial automotive market bypassing the years it would take otherwise. As Indian startups have shown too, companies with promise attract funding from foreign majors. Therefore, it is imperative that incubators are available to sprout ideas.

Why strategic independence in the electronics sector is so important

Let’s face it. High-tech imports are highly expensive and come with no transfer of technology. Critical tech is typically denied and only when domestic capability reaches near maturity, foreign OEMs and governments fall over themselves to offer sweet deals in a bid to prevent domestic programs from reaching fruition. This tactic has been used too many times, for it to be ignored.

Western countries focus on patents regime, IPR protection, access to domestic market, stringent opposition to import substitution and preference to local manufacturing under the guise of “difficulty for local manufacturing to access and leverage glocal hardware and software development chains”. These are simply aimed at putting India at a significant disadvantage, nothing more, nothing less.

Even as foreign players denounce India’s PMA, their home countries remain as protectionist as ever. In the US, from 1933 till date, price preference is given to US companies and import duties on some of the covered products are relatively high in some markets. Again in the US, applied duties on certain parts of telephone handsets are at 8.5 percent. In China, a 35 percent duty is applicable to video camera imports. The EU tariff applied on DVD recorders is 14 percent and Thailand applies a duty of 30 percent on certain magnetic cards. The US government is also mandated to report to the Senate on any waivers and has to justify each case. Similarly, in China for items like medical stents, procurement is deliberately skewed towards local products in local hospitals. Cheaper Chinese stents are making inroads in India after their price was capped stymieing in-country innovation generation.

Let us also not forget, that telecom equipment like all digital hardware is susceptible to foreign surveillance and interception. Given how much of the product ecosystem exists outside the country, it is only natural to assume so. With domestic manufacturers and even government bodies falling over themselves to rush to Huawei on study tours about 5G it will not be a major leap to see them enthusiastically import smart cities tech too. Telecom companies and business outreach groups have also opposed stricter testing and regulation norms. As we move further and further into a digital future with IoT gaining greater traction, prompted by greater wealth and better connectivity, the security aspect needs to be given a long hard look. Given the immense security challenges that they can bring forth, it is imperative that warnings are not drowned out as mere scaremongering.

It is every country for herself on the international stage and while “aid” might be forthcoming in times of need, it is in times of peace and stability that one must build the foundations of one’s prosperity. And Security.

© Delhi Defence Review. Reproducing this content in full without permission is prohibited.